Mis-sold PPI (Payment Protection Insurance)

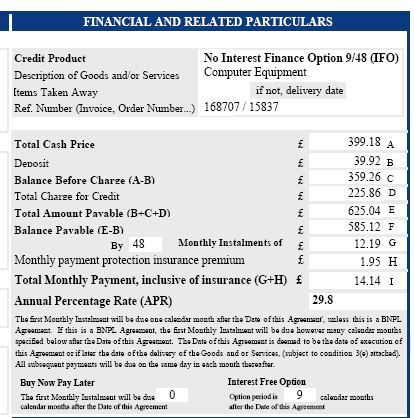

In this repayment plan that I took out in August 2004, offered by Scan Computers as a 0% interest deal, the PDF shows £1.95 in monthly PPI payments, which I never asked for and would certainly have declined. When the PDF was printed, so I could sign and return it, this PPI entry was blacked out. In fact, I didn't even notice this slight discrepancy in the monthly payment until a week ago, and that's when I discovered the mention of a PPI charge on the on-screen view of the PDF agreement.

I have sent a letter to Halifax Cetelem Credit Ltd, stating:

I should like to draw your attention to the amount of £1.95 payable each month which I have recently discovered is P.P.I. (Payment Protection Insurance). The credit agreement form I completed, signed and returned to you did not state that this amount was PPI, and I certainly would not have knowingly agreed to pay PPI.I therefore wish to discontinue this payment of P.P.I., and also enclose a cheque for £288.56 to cover the balance outstanding on this agreement (ignoring the erroneous PPI charges). I trust you will accept your mistake in these PPI charges, and that the cheque clears the outstanding balance.

As far as I am concerned, this is the end of the matter. However, I am sure that most people would not notice this "skimming" of cash to turn the 0% deal into a profit. Even if you aren't offered PPI, it may already be included anyway - so check the numbers carefully!

Another gotcha I had to be careful with, was the time window for which 0% interest applies. It doesn't apply for the length of the agreement, and in fact I'd start paying a whopping 29% interest on the remaining balance after nine months. Note that this agreement spans 48 months, so for over three years I'd be paying a colossal interest rate!

April 2011 Update: Finance companies are now being told to re-check all finance plans they've sold with bundled PPI, to identify whether the payment insurance was appropriate. There doesn't even need to have been a complaint from the consumer, so this could be a massive head-ache and resource drain for the companies. Given my experience of PPI being tacked on in a shady, underhand way, I say "Tough luck!"